Crypto assets have largely been coined with the general term “cryptocurrencies,” but to what degree do they actually act as a currency? Increasingly, crypto assets are functioning not as currencies but assets granting their owners ownership and governance of open-source blockchain technology that is able to capture quantifiable value. This is true at both the infrastructure and application layers. Many of these projects are attracting real cash flows and managing balance sheets in a decentralized manner. How all of this creates value for tokenholders can be easily misunderstood. This is the first post in a series that seeks to explain how crypto asset tokens accrue value. We will use Runa’s proprietary sector framework to break down the market and walk through one sector in each post. Part 1 will focus on the DeFi sector.

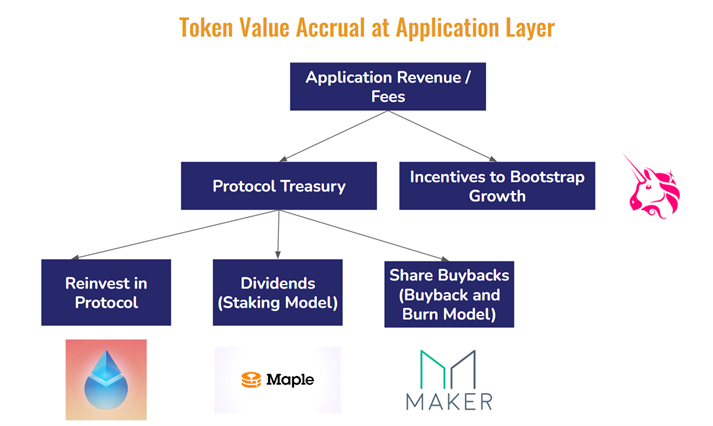

While most DeFi applications operate much differently than traditional businesses, many commonly used value creation strategies align. Just as it is a goal for businesses to increase enterprise value, DeFi applications attempt to increase the value of their project represented by their token. How do these tokens accrue value? Today there are four main strategies that projects use to re-allocate the value they capture: incentives to bootstrap growth, reinvesting in the protocol, staking distributions, and the buyback-and-burn model. Throughout this article, we will break down each model, as well as provide examples of projects that are utilizing each respective strategy.

Incentives to Bootstrap Growth

When growing a company, there are often tradeoffs between capturing profits early or keeping prices low to attract more customers. While it is tempting to focus on purely building revenue, bootstrapping growth and establishing a customer base are essential to the long-term success of a project. A recent and likely familiar example of this is the rideshare wars between Uber and Lyft. Both heavily discounted rides for users in order to capture an outsized share of the market. The strategy relied upon the belief that discounting rides would kickstart demand and drivers would consolidate their service to the dominant platform. This strategy does not return profits to investors and oftentimes means forgoing profits altogether, but it can be a catalyst for long-term price appreciation due to growth.

As the digital asset industry is nascent, many projects are in this high growth mode. Due to the wide array of options available to DeFi users, cementing returning users is essential for a growing project. The growth of a project’s fundamentals such as daily active users is likely to have a positive impact on the underlying token.

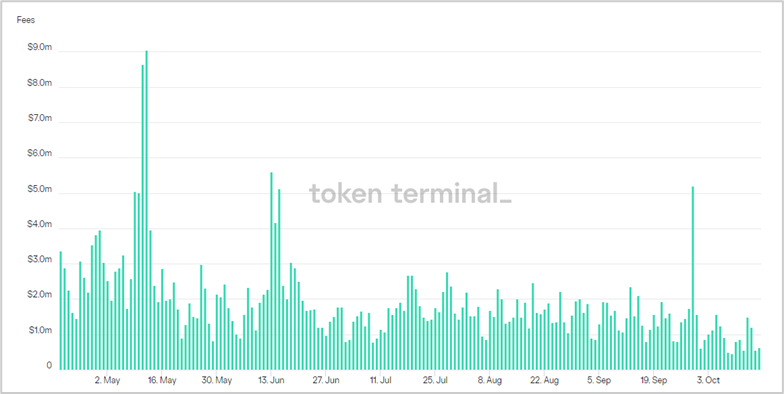

The decentralized exchange (DEX) market is massive ─ handling over $65 billion in trading volume just last month. DEXs earn revenue in the same way centralized exchanges do, by charging trading fees to users. On Uniswap, the largest DEX by volume, the standard fee is 0.30% of the notional value of the trade. A $1,000 trade generates $3 in revenue. As Uniswap attracts more volume, revenue increases.

A DEX is only able to be successful if it can attract a surplus of liquidity providers to meet trading demand for various pairs. As the saying goes, liquidity begets liquidity. To attract liquidity providers, Uniswap has decided to pass through all of the revenue generated from trading fees to those who add liquidity on the exchange. Going back to the Uber/Lyft analogy, this would be similar to Uber passing through 100% of rider fees to the driver. Uniswap’s token UNI is frequently critiqued for being “just a governance token,” only used to manage the DAO (decentralized autonomous organization) which controls the Uniswap application. While this is true today, in the future they could begin to share revenue with token holders. In fact, this is being actively debated on UNI governance forums.

Uniswap Daily Revenue

Source: token terminal. As of 10/16/2022.

Reinvesting in the Protocol

In an early-stage company, it is often necessary for the company to withhold profits to reinvest in development instead of yielding excess returns to stakeholders. While this doesn’t immediately benefit investors of the company, this profit retention and potential reinvestment help the project improve its market position and be poised for growth opportunities. This is often referred to as “growth mode” for a start-up because it allows the project to have gunpowder ready for future developments. Amazon has displayed an almost flawless execution of this strategy. Jeff Bezos outlined his thinking in his 1997 letter to shareholders, It’s all about the long term.

Many decentralized applications have begun to establish DAO treasuries, similar to balance sheets, that are managed through token holder governance. These treasuries can act both as a funding mechanism for growth and to backstop economic risk managed by the application. Oftentimes the establishment of the treasury is initially funded by allocating tokens to the DAO treasury at the token generation event. Some applications have also chosen to pass through a portion of their revenue to the treasury to grow the value of the DAO. Lido is a DeFi application that is using this path to strengthen the value of the LDO token.

With the rise of Proof of Stake (PoS) blockchains, a new sector of DeFi around liquid staking has become a popular solution for providing capital to node operators, while letting users utilize their funds. Lido allows users to deposit ETH to the platform to be used to run Ethereum validator nodes and earn the ETH staking yield. Lido then provides them tokens pegged to their deposit (deposit receipt). This is significant because users can then use these pegged tokens in other DeFi applications while still earning the ETH staking yield.

Lido acts as a service provider to its customers by providing the infrastructure to stake ETH while maintaining liquid utility through its pegged token, stETH. Of all yield earned by stakers on the platform, Lido takes a 10% fee, from which half goes to its infrastructure partners and half goes to the Lido treasury. With this 5%, the Lido treasury is able to grow in correlation with how much the platform is being used. The current treasury value is about $350 million, while the circulating market cap of LDO is a little over $630 million.

This treasury of funds is similar to a company’s book value, giving the LDO token value. Since the direction of the treasury is managed by LDO token holders, the bigger the treasury becomes, theoretically, the more powerful it is to hold LDO. Additionally, this treasury is largely used to fund improvements to the application through development, research, legal, marketing, and liquidity mining. The ability to influence the Lido project and the potential to receive future benefits as a token holder gives LDO value.

Staking Distributions

There are many ways to return capital back to shareholders and dividends are one of the most common and effective choices since it is a direct distribution of capital. In digital assets, dapps have gotten creative about ways to enable token holders to directly participate in the growth of the protocol by developing a model similar to that of a dividend.

Before describing this path of value accrual, we should first differentiate staking at the application layer from blockchain staking. Staking is most commonly referred to at the blockchain or base layer when describing participating as a validator for a Proof of Stake blockchain. As a reward or incentive for validating transactions for the network, stakers earn yield as highlighted in the Lido/Ethereum example above. role of staking at the application layer tends to vary widely from application to application and in each case brings different risks and rewards. For now, we are focused on application staking but in a later post, we will dive into how tokens in Runa’s Protocol sector accrue value through staking.

Each application implements a unique role for stakers in supporting their application. In some cases staking tokens involves the acceptance of additional risks not borne by non-stakers. In other cases, staking does not mean undertaking additional risks from the application and is a passive activity meant to reward long-term holders of the token. In both cases, the application incentivizes participation as a staker by distributing a portion of its earnings to those that have staked their tokens.

Let’s review an example of this model of token value capture which is currently utilized by Maple Finance, a DeFi lending and borrowing application.

Maple Finance is an infrastructure provider for debt capital markets on the Ethereum and Solana blockchains. Their business model is similar to debt issuers in traditional markets – for each loan originated on their application, they charge a 1% loan origination fee of which 66bps is revenue for Maple. The other 33bps goes to the loan underwriter (Pool Delegate).

With Maple’s 66bps of revenue, they have chosen to distribute 50%, or 33bps, back to token holders in the form of a dividend. To earn this dividend you must stake your Maple into a smart contract which accrues the dividend. Through this staking mechanism, the economics of the application are now connected to the token. As application revenue grows, the dividend yield of the token begins to increase.

Maple Staking Details

Source: maple.finance. As of 10/16/2022.

As you see above, staked maple holders (xMPL) currently earn a 2.83% APY on their holdings from staking distributions which come from application revenue. Maple’s tokenomics do not require xMPL holders to bear any additional risk (other than smart contract risk) associated with the application. Other DeFi tokens that use this model of token value accrual include SushiSwap and AAVE. In AAVE’s case however, staked token holders take on additional risk by serving as the first-loss capital if AAVE lending pools become undercollateralized.

Buyback-and-Burn

Another common method used by corporations in returning capital back to shareholders is using cash flow to repurchase outstanding shares in the open market. As a shareholder, you benefit by either selling your shares back to the issuer or from having your ownership percentage increase as the outstanding share count decreases. This has become a very popular method in TradFi with share repurchases reaching a record $881 billion in 2021 by S&P 500 stocks. Dapps have recreated this model through what is called a buyback-and-burn. The DAO (decentralized autonomous organization) which controls the dapp will set parameters that when met, will result in purchasing tokens from the open market. The tokens purchased are then “burnt” by a smart contract that destroys the tokens. The net result is a decrease in the token supply of the dapp.

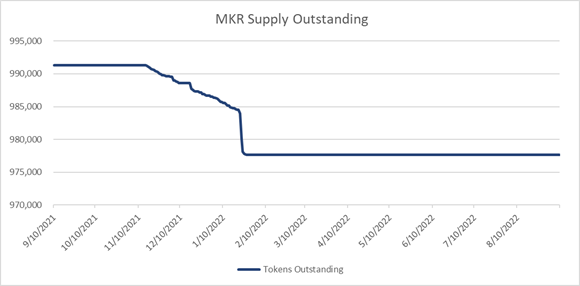

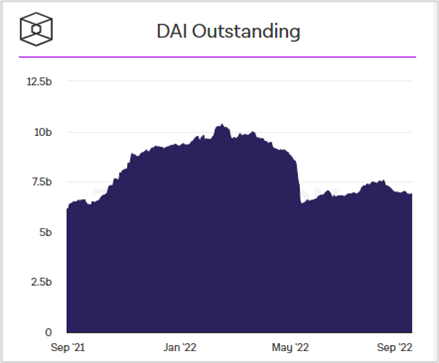

MakerDAO is a DeFi dapp that issues a stablecoin, DAI, using collateralized debt positions. DAI was one of the first stablecoins to market and today has ~$7B outstanding. Ownership of the MakerDAO is represented by the MKR token. Users interact with MakerDAO to generate the DAI stablecoin which is accepted across many web3 applications. A user locks collateral into a vault to generate DAI. MakerDAO charges a small fee on the vaults created by users, otherwise known as the stability fee. Stability fee revenues accrue directly to the MakerDAO balance sheet. Once a desired amount of cash is accrued to the balance sheet, MakerDAO begins to use cash flow from stability fees to repurchase outstanding MKR tokens.

MKR Tokens Outstanding

Period: September 10, 2021 – September 10, 2022. Source: Messari

DAI Outstanding

Period: September 10, 2021 – September 10, 2022. Source: The Block

Conclusion

Entrepreneurs and DAO’s continue to innovate and structure tokenomics that ensure the value created by applications flows through to token holders. The four models explained in this post are the most common in the DeFi sector but not comprehensive. We should also mention, the choice is not singular and dapps are oftentimes using multiple paths to create value for token holders regardless of time horizon.

Some dapps remain solely focused on building two-sided demand (UNI) and are less focused on short-term value for token holders. Others are amassing large treasuries (LDO) that will eventually be allocated towards further application development but for now, can be viewed as growing book value. A few projects have built-in mechanisms to pass through value (MPL, MKR) from the application to token holders.

At Runa, we invest with a long-term horizon and believe blockchain applications are only in their earliest stages of adoption. If you share this view, optimizing for the long-term growth of the project should be prioritized over returning capital to investors. However, it is important to build with a path to value capture in mind. As we are now seeing in other markets, investors are rewarding profitability over growth rates.

Special thank you to Charlie Perkins who co-authored this report.